Loans

Buying Property Without Selling Your Bitcoin: A New Strategy for Australian Investors

12 Mar 20263min

Australia’s property market is notoriously competitive. Meanwhile, a growing cohort of Australians have built significant wealth in digital assets like Bitcoin and Ethereum.

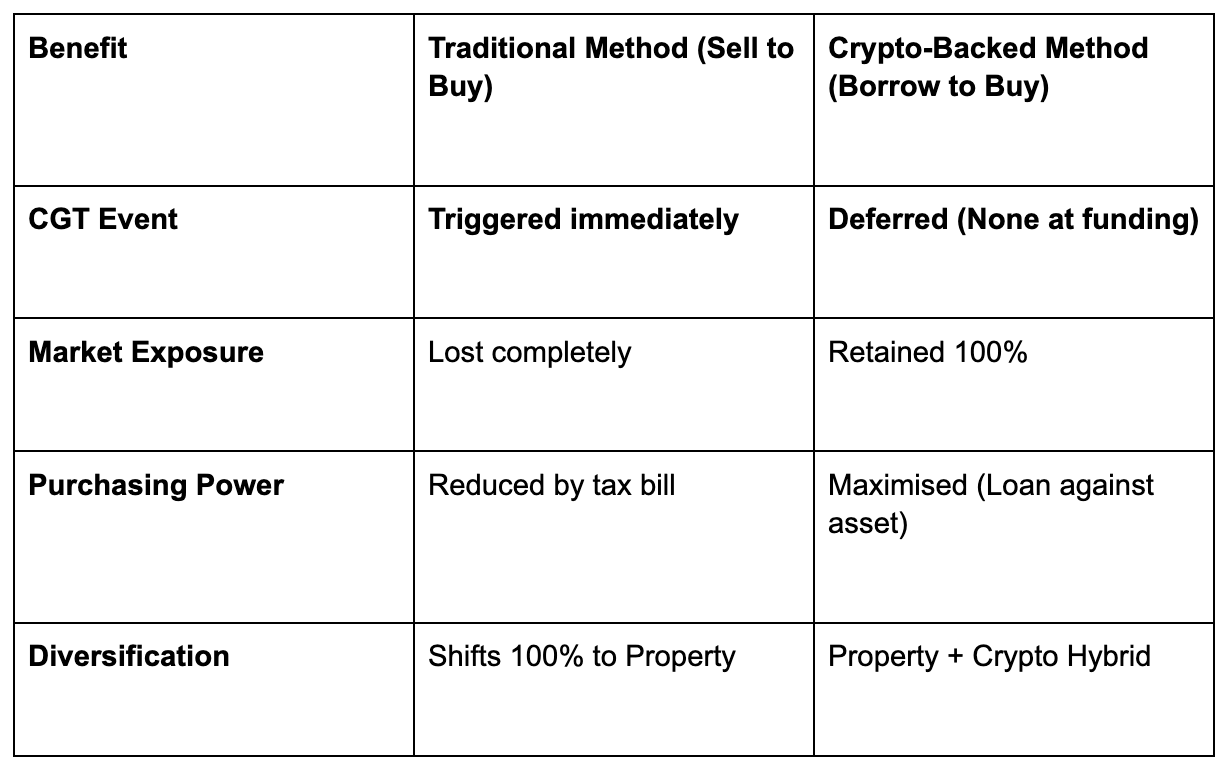

For years, these two asset classes were incompatible. To move from crypto to real estate, investors faced a "wealth paradox": they were asset-rich but cash-poor. To fund a deposit, they had to sell their crypto, triggering a massive Capital Gains Tax (CGT) event and destroying their long-term investment position.

That equation has changed. A new financial model—the crypto-backed home loan—now allows Australians to use digital assets as security, unlocking property ownership without the tax sting of liquidation.

The Problem: The "Tax Trap" of Selling Crypto

For long-term crypto holders, selling assets to fund a property purchase is often strategically disastrous.

When you dispose of cryptocurrency to buy a home, you trigger a "taxable event." In Australia, if you have held that asset for years, the resulting tax bill can wipe out a significant portion of your purchasing power.

Why selling is inefficient:

-

Immediate Tax Liability: You lose up to 45% (or 23.5% with the CGT discount) of your gains to the ATO immediately.

-

Loss of Market Position: You exit the market completely, missing out on potential future compounding.

-

Re-entry Risk: If you want to buy back in later, you may be forced to do so at a much higher price.

Banks traditionally do not recognise crypto wealth, leaving liquidation as the only option. Crypto-backed lending offers a sophisticated alternative.

What Is a Crypto-Backed Home Loan?

Definition: A crypto-backed home loan is a financing structure where a borrower pledges digital assets (like Bitcoin) as security to obtain Australian Dollars (AUD) for a property purchase, without transferring ownership of the crypto assets.

Instead of selling your Bitcoin to pay for a house, you use it as leverage.

1. You Deposit: You place your crypto into Fireblocks custody.

2. You Borrow: The lender provides AUD liquidity based on a Loan-to-Value Ratio (LVR).

3. You Buy: You use the cash to fund your property deposit or purchase.

4. You Hold: Because you haven’t sold, no Capital Gains Tax event is triggered at the time of funding.

This bridges the gap between the digital economy and the real-world property market.

The Solution: Block Earner’s Crypto-Backed Home Loan

Block Earner has pioneered this model in Australia, operating within a framework designed for regulatory compliance and security. It is currently the primary route for Australians to access this type of hybrid finance.

How the Structure Works

Unlike speculative DeFi lending, this is a structured financial product designed for real estate:

-

Security: You deposit approved assets (e.g., BTC, ETH).

-

LVR Assessment: Loans are issued based on a safe Loan-to-Value Ratio to manage volatility risk.

-

AUD Funding: You receive AUD directly, which can be used for a deposit or full settlement.

-

Ownership: You remain the beneficial owner of the cryptocurrency.

By using this model, investors can effectively "double-dip": they retain the potential upside of their crypto portfolio while simultaneously gaining exposure to the Australian property market.

Who Is This Strategy Suitable For?

This financial product is not for day traders; it is designed for high-conviction, long-term investors. It is particularly effective for:

-

Long-term HODLers: Investors with significant unrealised gains who want to avoid a CGT trigger.

-

Crypto-Paid Professionals: Founders and contractors who earn income in crypto and lack traditional payslips.

-

Asset-Rich, Cash-Poor Buyers: Individuals with millions in digital assets but limited AUD liquidity for a bank deposit.

-

Diversifiers: Investors looking to rebalance their portfolio into "safe haven" real estate without exiting their high-growth digital positions.

Strategic Benefits at a Glance

The Application Process: From Wallet to Keys

The process is designed to mirror a standard lending experience, but with digital assets as the engine:

1. Assessment: Apply using personal/entity details.

2. Crypto Security: Transfer digital assets to the custodian.

3. Valuation: LVR is calculated, and loan terms are issued.

4. Settlement: AUD funds are released for the property transaction.

5. Repayment: Pay down the loan over time (or pay it off by selling crypto later in a more tax-advantageous year).

Conclusion: A Bridge Between Two Worlds

Crypto-backed home loans represent the maturation of the digital asset market in Australia. For the first time, digital wealth can be treated as real financial capital.

For our clients, the ability to unlock liquidity without liquidation is a powerful tax planning tool. It allows for the acquisition of lifestyle or investment property without sacrificing the investment thesis that built the wealth in the first place.

Block Earner is currently leading crypto-backed loan and bitcoin-backed loan infrastructure in Australia. If you are sitting on significant digital gains and looking to enter the property market, this is a conversation worth having.

Frequently Asked Questions (FAQ)

Does a crypto-backed loan trigger Capital Gains Tax? Generally, no. Because you are pledging the asset as security rather than disposing of it, a CGT event is typically not triggered at the time of the loan. However, tax laws are complex, and you should seek personal advice.

What happens if the price of Bitcoin drops? Like any secured loan, margin requirements apply. If the value of your crypto security drops significantly, you may need to top up your crypto security or repay part of the loan to maintain a healthy Loan-to-Value Ratio (LVR).

Is Block Earner regulated in Australia? Yes. Block Earner operates within Australian regulatory frameworks, complying with AML/CTF (Anti-Money Laundering and Counter-Terrorism Financing) standards to ensure a safe lending environment.

Disclaimer: The information contained in this blog is general in nature and is provided for informational purposes only. It does not constitute financial, legal, or tax advice, and should not be relied upon as such. Block Earner does not guarantee the accuracy or completeness of any information presented. You should consider your own personal circumstances and seek professional advice before making any financial or investment decisions. Past performance is not indicative of future results. All investments carry risk.