Loans

Crypto-Backed Loans: The Alternative to Selling Your Bitcoin Before the 2027 CGT Changes

Table of contents

- The starting point: original investment

- What changes on 1 July 2027

- The alternative: borrow against your Bitcoin instead of selling it

- Comparing loan costs to the tax on a sale

- What happens when you factor in Bitcoin's growth

- What to watch out for

- The bottom line

Key takeaways

-

From 1 July 2027, the 50% CGT discount will be replaced by cost-base indexation with a 30% minimum tax rate on capital gains.

-

For a $10,000 Bitcoin gain on a position that doubled in a year, top-bracket investors could pay close to twice as much tax under the new rules ($4,559 vs $2,350).

-

Borrowing against a Bitcoin position is one alternative to selling it. The holder retains market exposure to both upside and downside.

-

At Block Earner's effective 11.93% comparison rate, cumulative loan costs equal the tax payable on an equivalent sale somewhere between 2.4 and 3.8 years, depending on the borrower's marginal rate.

-

Crypto-backed loans carry risks and tax outcomes are individual. Professional advice should inform any sell-vs-borrow decision.

Australia's 2026-27 federal budget quietly proposed one of the biggest changes to investor tax in a generation. From 1 July 2027, the 50% Capital Gains Tax discount most Australians take for granted will be replaced by an inflation-indexed system, with a minimum 30% tax floor on capital gains.

For Bitcoin holders sitting on years of appreciation, the maths shifts meaningfully. But there's an alternative that's been used by wealthy investors for decades that doesn't require selling, and Block Earner's Crypto-Backed Loans now make it accessible to everyday holders.

Let's walk through the numbers.

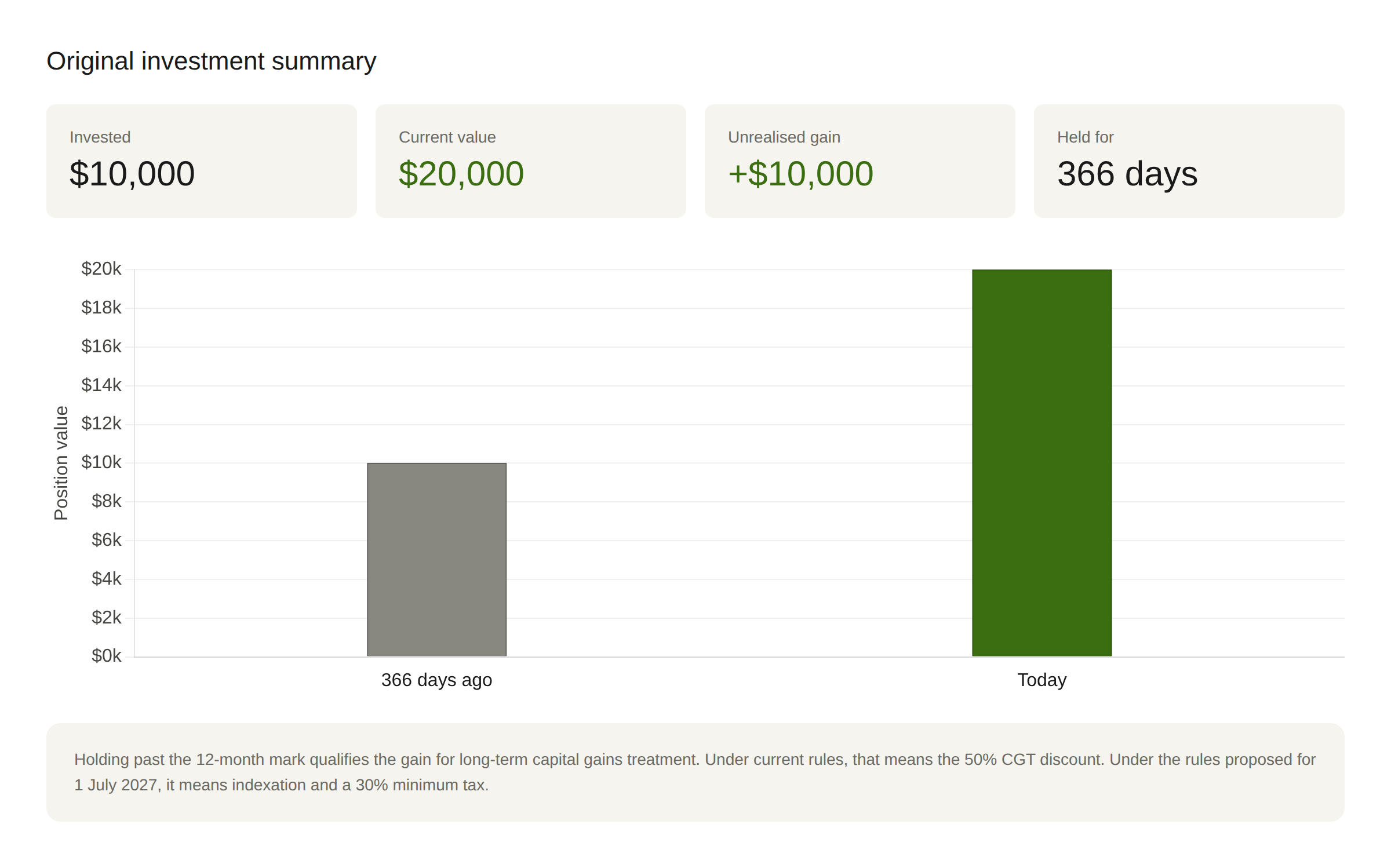

The starting point: original investment

Imagine you bought $10,000 of Bitcoin just over 12 months ago. Today it's worth $20,000. A clean double, the kind of return that made Bitcoin famous.

You're now sitting on a $10,000 capital gain, and the asset has been held for more than 12 months, so under current rules, you qualify for the 50% CGT discount. So far, so familiar.

What changes on 1 July 2027

The current system is simple: hold an asset for more than 12 months, pay tax on half the gain at your marginal rate. The new system replaces that with two changes working together.

Cost base indexation

Instead of halving the gain, your original purchase price gets adjusted upward for inflation. You're taxed on the "real" gain, what's left after stripping out inflation. For a Bitcoin position that doubled in a year, indexation barely moves the needle (roughly $300 on a $10k cost base at 3% CPI). The taxable amount stays close to the full $10,000 gain.

30% minimum tax rate

Even if your marginal rate is lower, capital gains get taxed at a minimum of 30%. This was designed to stop high earners deferring sales until retirement, but it catches anyone in a sub-30% bracket too.

The combined effect: for assets that appreciated faster than inflation, which describes most long-term Bitcoin holders, the new system results in a materially higher tax bill.

At the top marginal rate, the tax on your $10k Bitcoin gain nearly doubles, from $2,350 under the current rules to $4,559 under the new system. Even middle-income earners pay roughly twice as much.

There's a window. The new rules only apply to gains accruing after 1 July 2027. Gains realised before that date still get the 50% discount. Assets held across that date use a hybrid calculation based on the asset's value on 1 July 2027.

So one option is to sell before the deadline. But for long-term Bitcoin holders, selling means leaving the asset behind entirely, and historically, holders who didn't sell during volatile periods have been rewarded over multi-year horizons.

The alternative: borrow against your Bitcoin instead of selling it

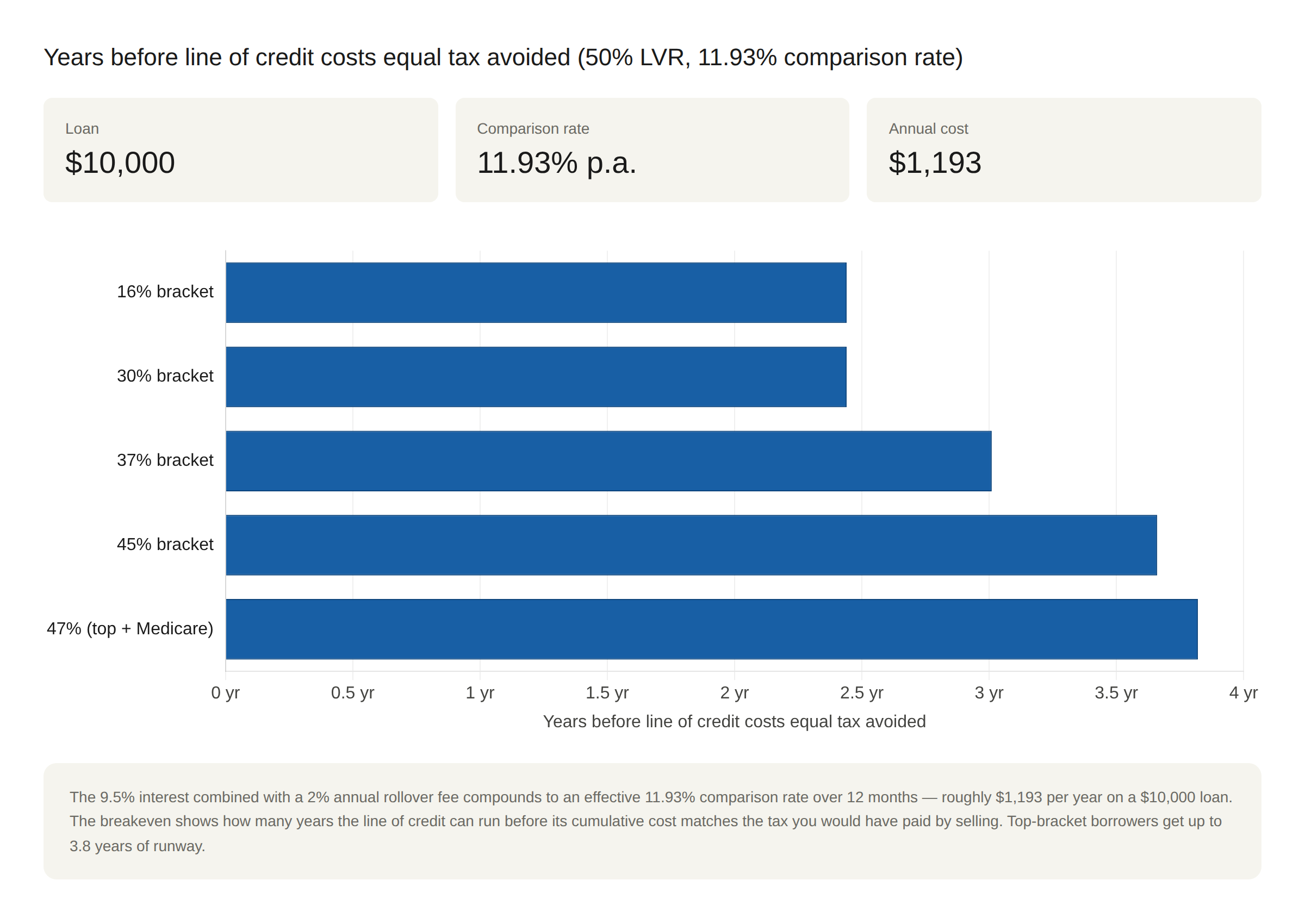

There's a different way to access the value sitting in your Bitcoin. Block Earner's crypto-backed line of credit lets you borrow against your holdings at a 9.5% interest rate, with a 50% loan-to-value ratio and a 2% annual rollover fee. If you don't make repayments during the term, those costs compound to an effective 11.93% comparison rate over the 12-month line of credit.

Here's the key insight: borrowing against an asset is not the same as selling it. You retain ownership of the Bitcoin and maintain your market exposure, to both upside and downside.

On a $20,000 Bitcoin position, that's up to $10,000 in liquid cash, with an effective annual cost of around $1,193 if no repayments are made during the term.

Comparing loan costs to the tax on a sale

This is the core question. If borrowing costs eventually exceed the tax that would have been payable on a sale, the cost-benefit shifts. So we calculated the breakeven for each tax bracket, the point at which cumulative loan costs equal the tax you would have paid by selling.

The answer ranges from 2.4 years for lower-income borrowers to 3.8 years at the top marginal rate. Higher earners get a longer runway because the tax they'd otherwise pay is larger.

But this is the conservative case. It assumes Bitcoin holds completely flat the entire time you have the loan. In reality, the asset's value will move with the market, and historically, it has moved up over multi-year periods.

What happens when you factor in Bitcoin's growth

Bitcoin's compound annual growth rate over the last seven years has been roughly 57%, a number heavily inflated by 2020's 303% surge, but extraordinary even after smoothing. Even modelling Bitcoin at just 20% per year, about a third of the historical rate, changes the picture entirely.

By year seven, even at a deliberately conservative 20% CAGR (Compound Annual Growth Rate), the borrower's net position is roughly double what the seller ends up with after investing their after-tax cash at 7%. At Bitcoin's historical growth rate, the borrower ends up with around 20× more wealth.

The reason is simple: the loan costs grow linearly while a held Bitcoin position can compound if prices rise. A few thousand dollars of annual fees are rounding error against an asset that's grown 50× over the last decade.

What to watch out for

Not all crypto-backed loan providers are the same. Before borrowing against your crypto, look for clear risk disclosures, check where the company is based, understand which regulatory jurisdiction it operates in, and consider seeking independent professional advice.

Volatility and margin calls

Bitcoin's 2022 drawdown was 64%. A loan at 50% LVR provides a meaningful buffer against drawdowns, but extreme moves can still trigger margin calls.

Block Earner notifies you as your LVR rises toward the default notice threshold, via email, in-app and SMS, giving you time to top up your crypto security or repay AUD to restore your loan health. If no action is taken and your LVR remains too high, Block Earner may sell a portion of your crypto security to bring the loan back to a healthy level.

Deductibility

Whether loan interest is tax-deductible depends on how you use the borrowed funds. Generally, interest is only deductible if the loan is used to generate assessable income. Borrowing for personal consumption typically isn't deductible. Talk to your accountant.

Legislation isn't final

The new CGT changes were announced in the 2026 federal budget but require parliament to pass them. Final detail may change.

Past performance

Bitcoin's historical CAGR is real, but it doesn't guarantee future returns. The cost-benefit of borrowing versus selling depends on how the asset performs over your holding period.

The bottom line

For Australians who believe Bitcoin will continue to grow, and who have meaningful unrealised gains, the 2026 budget changes have made the "sell vs borrow" decision much more consequential.

Selling crystallises a tax bill that's about to get materially larger. Borrowing at an effective 11.93% maintains your market exposure, to both upside and downside. That's a risk worth understanding before entering. The breakeven maths gives you between 2.4 and 3.8 years of pure cost runway. If the underlying asset appreciates, that runway extends further.

Block Earner's crypto-backed loans give holders the option to access liquidity against their position rather than sell it. Whether that's the right choice depends on your circumstances, your view on the asset, and your tax position, which is why professional advice matters.

Disclaimer: Tax outcomes are individual. Always seek independent tax advice. This article describes a general framework, not a tax strategy specific to your circumstances. Whether a loan-versus-sale decision results in a better overall outcome depends on your marginal rate, asset basis, holding period, intended use of funds, and the eventual exit point of the position. The information contained in this blog is general in nature and is provided for informational purposes only. It does not constitute financial, legal, or tax advice, and should not be relied upon as such. Block Earner does not guarantee the accuracy or completeness of any information presented. You should consider your own personal circumstances and seek professional advice before making any financial or investment decisions. Past performance is not indicative of future results. All investments carry risk. Crypto-backed loans carry real risks. The value of your crypto can fall sharply, rapidly increasing your LVR and reducing any initial buffer. This may require you to add security or repay part of the loan and could result in some or all of your crypto being sold.

Approved applicants only. Terms, conditions, fees and charges apply. The rate provided above is indicative and your rate may be different based on a variety of factors, including your credit worthiness. Rates are subject to change. ^The comparison rates are based on a secured loan of $10,000 over a term of 3 years. The comparison rate provided includes a 2% origination fee. WARNING: This comparison rate is true only for the examples given and may not include all fees and charges. Different terms, fees or other loan amounts might result in a different comparison rate. Credit provided by Web3 Loans Pty Ltd ACN 668 516 952 and managed by Web3 Ventures Pty Ltd trading as Block Earner (ACN 655 090 869) under Australian Credit License 542689. Capital is not covered by the Australian government deposit guarantee.